Gold Wavers Amid Market Euphoria

July 11, 2023

Read Time 6 MIN

Monthly gold market and economic insights from Imaru Casanova, Portfolio Manager, featuring her unique views on mining and gold’s portfolio benefits. An expanded PDF version of this commentary, including fund specific information can be downloaded here.

Not the dollar this time…

Gold was down $43.38 per ounce or 2.2% for the month, closing at $1,919.35 on June 30. Two- and ten-year treasury yields climbed higher in June, but the U.S. dollar was not to be blamed for gold’s drop this time. The U.S. dollar index (DXY)1 was also down in June (-1.4%).

Instead, gold was pressured by the relentless strength of the U.S. equity markets, which were undeterred by the outlook for more rate hikes this year, or by the recession signals sent by the most deeply inverted treasury yield curve in decades. The S&P 5002 and the NASDAQ 1003 were both up more than 6.5% in June, posting double digit gains for the year with the tech-heavy NASDAQ up a whopping 39% in the first half of 2023. Apple closed the month at a milestone $3 trillion market cap, the world’s first company ever to reach such valuation.

A notable revision to first-quarter GDP annualized growth to 2% from 1.3%, along with other better-than-expected economic releases (e.g., U.S. May retail sales, housing starts, jobless claims, consumer sentiment), slowing inflation and comments from the U.S. Federal Reserve (Fed) chairman and Treasury Secretary downplaying the risk of a recession, likely fueled the optimism.

The NYSE Arca Gold Miners Index (GDMNTR)4 and the MVIS Global Juniors Gold Miners Index (MVGDXJTR)5 felt the pressure of a declining gold price, down 2.5% and 3.9% respectively during the month of June. Following what was a dreadful month for gold equities in May, we were pleased to see the equities performing much more in line with our expectations in June. We expect strong gold mining sector fundamentals in a year when average gold prices are at record highs ($1,934 in the first half of 2023), will lead to a progressive contraction of the valuation gap between the metal and the stocks.

Gold’s drivers still remain the same

Our outlook for higher gold prices in the longer term is unchanged, supported by the risks imposed by sustained elevated interest rates, sticky inflation, continued global geopolitical tensions, a trend by countries around the world to diversify away from the U.S. dollar and increase their gold reserves, and the pending risk of a U.S. and/or global economic recession. Investors continue to stay on the sidelines of the gold market. Global gold bullion ETF holdings, our proxy for investment demand, declined 1.64% during the month of June, leading to net outflows year-to-date of 1.21%.

Gold failed to hold above $1,950 per ounce. It may now trade sideways around the $1,900 level, until a new catalyst emerges. A Fed skip, signaling the nearing of the end of the tightening cycle, failed to provide impetus for gold and attract investors. But as the end of the hiking cycle approaches, the reasons for a pause (fear to launch the economy into a recession or into a deeper recession) and the implications on inflation, could become important gold price drivers.

SPECIAL – Walking on Gold: Junior Miners in the Alaska/Yukon Region

VanEck’s active gold strategy has always maintained a significant allocation to juniors. We divide our junior investments into producers, with mine production of up to 300,000 ounces per year, and developers, with properties under development that we believe can reach an economic reserve of at least two million ounces. We don’t invest in junior exploration stocks because we find them too speculative. While most explorers claim they’ve made a discovery, very few will ever meet our two-million-ounce threshold.

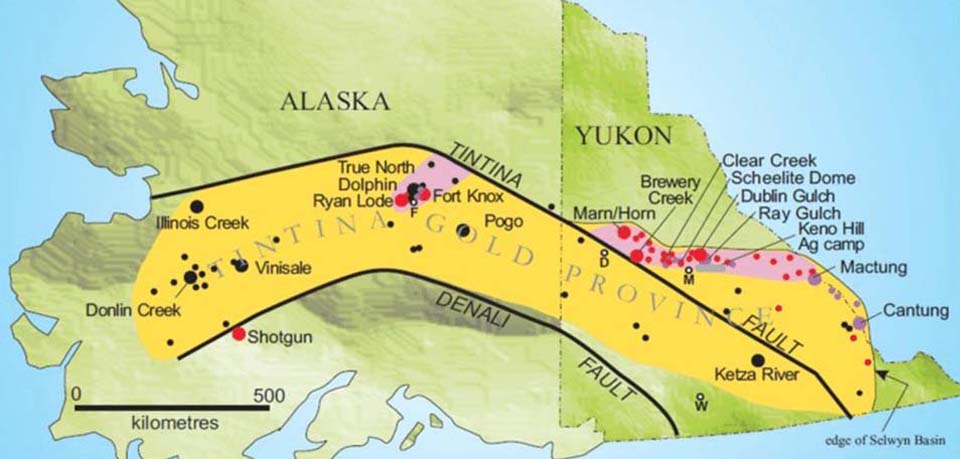

We often travel to exploration and development sites to help determine whether a property has the potential to meet our investment criterion. We recently spent time in the Yukon and Alaska to visit several promising projects in the Tintina Gold Province (yellow on map), where most of the gold deposits occur in and around Cretaceous (145 to 66 million years old) granitic intrusions scattered throughout the Tombstone Plutonic Belt (pink on map). The Tombstone Belt is about 70 miles wide and trends west-northwest through the Yukon. It is offset along the Tintina Fault, a major strike-slip fault that carried the western portion of the belt 300 miles to the northwest into Alaska during the Eocene Age (55.8 to 33.9 million years ago).

Map of Alaska’s Tintina Gold Province (yellow) and Tombstone Belt (pink). Source: Apex Geoscience Ltd. (May 2016).

Kinross’ Fort Knox mine is located in the Fairbanks gold district, Alaska in the western-most portion of the Tombstone Belt. Since 1996, Fort Knox has produced over 8 million ounces of gold from low-grade ores. We visited the Fairbanks district where Freegold Ventures (0.00% of Strategy net assets) is drilling its Golden Summit project. In February, Freegold announced a resource of 20.6 million ounces.i We also visited Banyan Gold’s (0.00% of Strategy net assets) AurMac property in the Mayo Gold district, Yukon. Banyan announced a 6.2-million-ounce resource in May.ii Both of these properties have good infrastructure with roads and power. However, both are low grade with resources under one gram per tonne (0.029 ounces per ton). The companies are working to further define the resources and their metallurgy (gold process/recoveries) in order to fully assess the economics.

At the eastern end of the Tombstone Belt we visited Snowline Gold’s (0.52% of Strategy net assets) Rogue property. Snowline announced the discovery of the Valley deposit in January 2022. While Snowline has yet to publish a maiden resource, drilling so far indicates that Valley is a multi-million-ounce deposit that crops out on surface. The photo shows Valley core drilled through a granodiorite intrusive that is riddled with gold-bearing sheeted quartz veins. This is classic Tombstone belt mineralization.

Gold-bearing core samples from Snowline’s Rogue property. Source: VanEck (June 2023).

Unlike Golden Summit and AurMac, Valley is remote. The camp is accessed by fixed wing aircraft and the Valley deposit is accessed via helicopter from there.

One of several small aircraft required to visit Snowline’s remote Valley deposit. Source: VanEck (June 2023).

Valley carries higher grades than most Tombstone belt deposits, but getting roads and power to the site will be a challenge. Snowline is working on the challenges while continuing to delineate Valley and explore other targets on the Rogue properties.

We reckon we walked over roughly 30 million ounces of undeveloped gold on our trip. Junior explorers and developers are the life blood of the gold industry. Explorers take the risks and developers do the work of taking a deposit from discovery to reserve and from permitting to production. Quality projects are often acquired by a larger producer along the way. Junior producer Victoria Gold (0.00% of Strategy net assets) and mid-tier producer B2Gold (4.32% of Strategy net assets) have taken strategic equity stakes in Banyan and Snowline respectively. This trip convinced us that there will surely be another major mine built along the Tombstone Belt.

To receive more insights to Gold Investing insights, sign up in our subscription center.

Follow Us

Important Disclosures

i Freegold Extends Mineralization 400 Metres To The North At Golden Summit.

ii Banyan Gold increases AurMac inferred ounces by over 50%.

All company, sector, and sub-industry weightings as of June 30, 2023 unless otherwise noted.

Please note that VanEck may offer investments products that invest in the asset class(es) or industries included in this communication.

This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results.

Nothing in this content should be considered a solicitation to buy or an offer to sell shares of any investment in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction, nor is it intended as investment, tax, financial, or legal advice. Investors should seek such professional advice for their particular situation and jurisdiction.

1The U.S. Dollar Index measures the value of the U.S. dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners' currencies. 2S&P 500 Index is a market-capitalization-weighted index of 500 leading publicly traded companies in the United States. 3NASDAQ 100 Index is a modified market capitalization weighted index comprising the 100 largest, most actively-traded U.S. companies listed on the Nasdaq stock exchange. 4NYSE Arca Gold Miners Index (GDMNTR) is a modified market capitalization-weighted index comprised of publicly traded companies involved primarily in the mining for gold. 5MVIS Global Junior Gold Miners Index (MVGDXJTR) is a rules-based, modified market capitalization-weighted, float-adjusted index comprised of a global universe of publicly traded small- and medium-capitalization companies that generate at least 50% of their revenues from gold and/or silver mining, hold real property that has the potential to produce at least 50% of the company’s revenue from gold or silver mining when developed, or primarily invest in gold or silver.

Any indices listed are unmanaged indices and include the reinvestment of all dividends, but do not reflect the payment of transaction costs, advisory fees or expenses that are associated with an investment in a Fund. Certain indices may take into account withholding taxes. An index’s performance is not illustrative of a Fund’s performance. Indices are not securities in which investments can be made.

Investments in commodities can be very volatile and direct investment in these markets can be very risky, especially for inexperienced investors.

NYSE Arca Gold Miners Index is a service mark of ICE Data Indices, LLC or its affiliates (“ICE Data”) and has been licensed for use by VanEck ETF Trust (the “Trust”) in connection with VanEck Gold Miners ETF (the “Fund”). Neither the Trust nor the Fund is sponsored, endorsed, sold or promoted by ICE Data. ICE Data makes no representations or warranties regarding the Trust or the Fund or the ability of the NYSE Arca Gold Miners Index to track general stock market performance.

ICE DATA MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND HEREBY EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE WITH RESPECT TO THE NYSE ARCA GOLD MINERS INDEX OR ANY DATA INCLUDED THEREIN. IN NO EVENT SHALL ICE DATA HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, INDIRECT, OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFITS), EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

MVIS Global Junior Gold Miners Index (the “Index”) is the exclusive property of MarketVector Indexes GmbH (a wholly owned subsidiary of Van Eck Associates Corporation), which has contracted with Solactive AG to maintain and calculate the Index. Solactive AG uses its best efforts to ensure that the Index is calculated correctly. Irrespective of its obligations towards MarketVector Indexes GmbH, Solactive AG has no obligation to point out errors in the Index to third parties. The VanEck Junior Gold Miners ETF (the “Fund”) is not sponsored, endorsed, sold or promoted by MarketVector Indexes GmbH and MarketVector Indexes GmbH makes no representation regarding the advisability of investing in the Fund.

The Gold Strategy is subject to the risks associated with concentrating its assets in the gold industry, which can be significantly affected by international economic, monetary and political developments. The strategy’s overall portfolio may decline in value due to developments specific to the gold industry. The strategy investments in foreign securities involve risks related to adverse political and economic developments unique to a country or a region, currency fluctuations or controls, and the possibility of arbitrary action by foreign governments, or political, economic or social instability. The strategy is subject to risks associated with investments in Canadian issuers, commodities and commodity-linked derivatives, commodities and commodity-linked derivatives tax, gold-mining industry, derivatives, emerging market securities, foreign currency transactions, foreign securities, other investment companies, management, market, non-diversification, operational, regulatory, small- and medium-capitalization companies and subsidiary risks.

Please note that the information herein represents the opinion of the author, but not necessarily those of VanEck, and this opinion may change at any time and from time to time. Non-VanEck proprietary information contained herein has been obtained from sources believed to be reliable, but not guaranteed. Not intended to be a forecast of future events, a guarantee of future results or investment advice. Historical performance is not indicative of future results. Current data may differ from data quoted. Any graphs shown herein are for illustrative purposes only. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

Diversification does not assure a profit or protect against loss.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.

Van Eck Securities Corporation, Distributor, a wholly owned subsidiary of Van Eck Associates Corporation.

666 Third Avenue | New York, NY 10017

Related Funds

Important Disclosures

i Freegold Extends Mineralization 400 Metres To The North At Golden Summit.

ii Banyan Gold increases AurMac inferred ounces by over 50%.

All company, sector, and sub-industry weightings as of June 30, 2023 unless otherwise noted.

Please note that VanEck may offer investments products that invest in the asset class(es) or industries included in this communication.

This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results.

Nothing in this content should be considered a solicitation to buy or an offer to sell shares of any investment in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction, nor is it intended as investment, tax, financial, or legal advice. Investors should seek such professional advice for their particular situation and jurisdiction.

1The U.S. Dollar Index measures the value of the U.S. dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners' currencies. 2S&P 500 Index is a market-capitalization-weighted index of 500 leading publicly traded companies in the United States. 3NASDAQ 100 Index is a modified market capitalization weighted index comprising the 100 largest, most actively-traded U.S. companies listed on the Nasdaq stock exchange. 4NYSE Arca Gold Miners Index (GDMNTR) is a modified market capitalization-weighted index comprised of publicly traded companies involved primarily in the mining for gold. 5MVIS Global Junior Gold Miners Index (MVGDXJTR) is a rules-based, modified market capitalization-weighted, float-adjusted index comprised of a global universe of publicly traded small- and medium-capitalization companies that generate at least 50% of their revenues from gold and/or silver mining, hold real property that has the potential to produce at least 50% of the company’s revenue from gold or silver mining when developed, or primarily invest in gold or silver.

Any indices listed are unmanaged indices and include the reinvestment of all dividends, but do not reflect the payment of transaction costs, advisory fees or expenses that are associated with an investment in a Fund. Certain indices may take into account withholding taxes. An index’s performance is not illustrative of a Fund’s performance. Indices are not securities in which investments can be made.

Investments in commodities can be very volatile and direct investment in these markets can be very risky, especially for inexperienced investors.

NYSE Arca Gold Miners Index is a service mark of ICE Data Indices, LLC or its affiliates (“ICE Data”) and has been licensed for use by VanEck ETF Trust (the “Trust”) in connection with VanEck Gold Miners ETF (the “Fund”). Neither the Trust nor the Fund is sponsored, endorsed, sold or promoted by ICE Data. ICE Data makes no representations or warranties regarding the Trust or the Fund or the ability of the NYSE Arca Gold Miners Index to track general stock market performance.

ICE DATA MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND HEREBY EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE WITH RESPECT TO THE NYSE ARCA GOLD MINERS INDEX OR ANY DATA INCLUDED THEREIN. IN NO EVENT SHALL ICE DATA HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, INDIRECT, OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFITS), EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

MVIS Global Junior Gold Miners Index (the “Index”) is the exclusive property of MarketVector Indexes GmbH (a wholly owned subsidiary of Van Eck Associates Corporation), which has contracted with Solactive AG to maintain and calculate the Index. Solactive AG uses its best efforts to ensure that the Index is calculated correctly. Irrespective of its obligations towards MarketVector Indexes GmbH, Solactive AG has no obligation to point out errors in the Index to third parties. The VanEck Junior Gold Miners ETF (the “Fund”) is not sponsored, endorsed, sold or promoted by MarketVector Indexes GmbH and MarketVector Indexes GmbH makes no representation regarding the advisability of investing in the Fund.

The Gold Strategy is subject to the risks associated with concentrating its assets in the gold industry, which can be significantly affected by international economic, monetary and political developments. The strategy’s overall portfolio may decline in value due to developments specific to the gold industry. The strategy investments in foreign securities involve risks related to adverse political and economic developments unique to a country or a region, currency fluctuations or controls, and the possibility of arbitrary action by foreign governments, or political, economic or social instability. The strategy is subject to risks associated with investments in Canadian issuers, commodities and commodity-linked derivatives, commodities and commodity-linked derivatives tax, gold-mining industry, derivatives, emerging market securities, foreign currency transactions, foreign securities, other investment companies, management, market, non-diversification, operational, regulatory, small- and medium-capitalization companies and subsidiary risks.

Please note that the information herein represents the opinion of the author, but not necessarily those of VanEck, and this opinion may change at any time and from time to time. Non-VanEck proprietary information contained herein has been obtained from sources believed to be reliable, but not guaranteed. Not intended to be a forecast of future events, a guarantee of future results or investment advice. Historical performance is not indicative of future results. Current data may differ from data quoted. Any graphs shown herein are for illustrative purposes only. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

Diversification does not assure a profit or protect against loss.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.

Van Eck Securities Corporation, Distributor, a wholly owned subsidiary of Van Eck Associates Corporation.

666 Third Avenue | New York, NY 10017