Who’s Afraid of High Interest Rates?

October 19, 2022

Read Time 2 MIN

Global Debt Service Costs

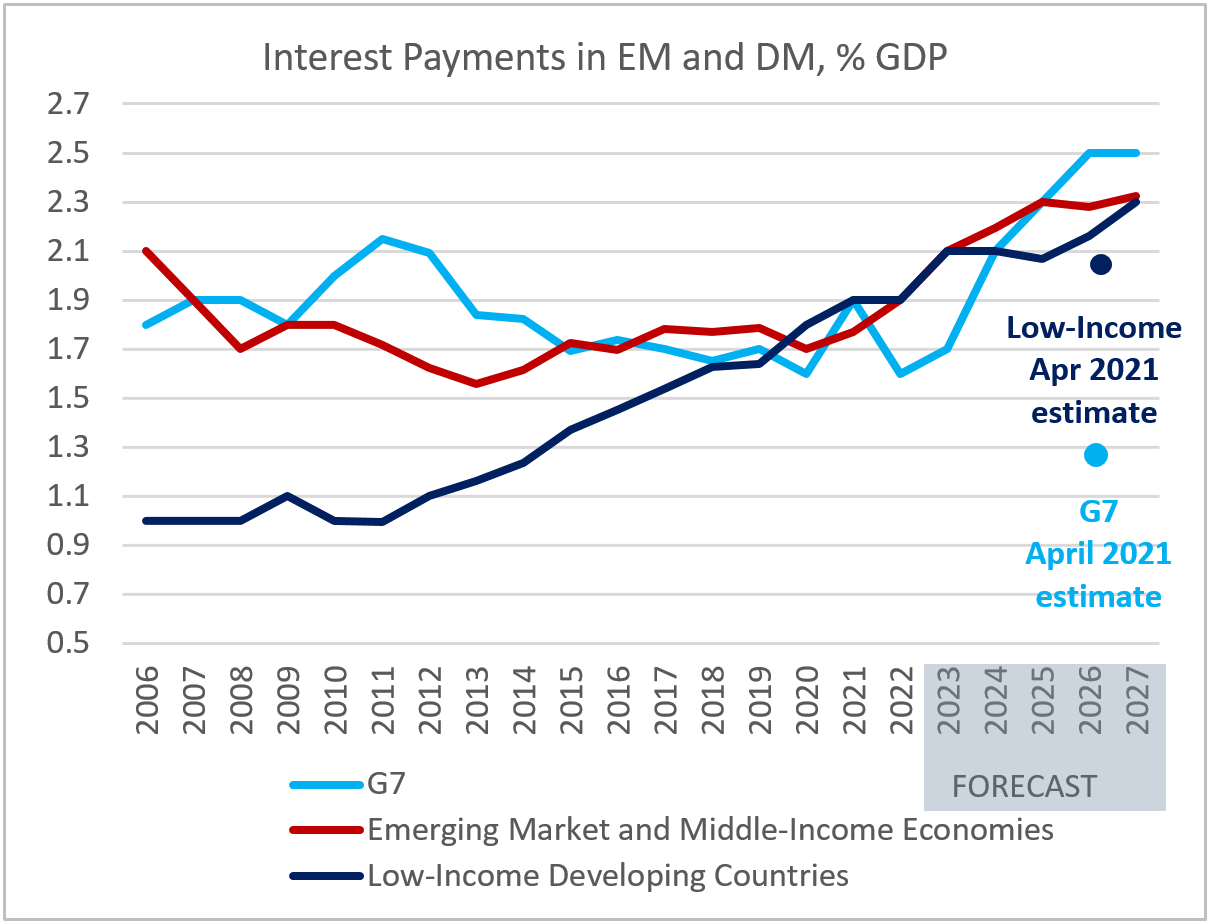

There are still no signs of China’s “delayed” activity indicators and foreign trade numbers this morning, and this gives us more time to study the latest batch of the IMF’s research reports – which contain not only updated growth forecasts, but also a lot of interesting stuff on global interest rates. Rising developed markets (DM) interest rates – the 10-year U.S. Treasury yields reached another post-2008 high this morning – mean that net interest payments in that part of the world can almost double in the next few years, compared to estimates made a year and a half ago (see chart below). This is not a DM debt sustainability crisis (yet) – nominal GDP growth is still well above nominal rates. However, DMs might no longer be “exceptional” in their ability to borrow without immediate consequences, which was the predominant view 1.5 years ago.

EM Inflation and Rate Hikes

The increase in the debt service costs in emerging markets (EM) – even though less surprising than in G7 – should also be monitored very closely. South Africa is among the countries where the IMF expects net interest payments to exceed 5% of GDP starting in 2023 (potentially reaching 6% of GDP and more from 2025 onwards). The government’s ability to control inflation and the central bank’s policy response are, therefore, of utmost importance. Today’s headline inflation surprised slightly to the downside, easing to 7.5% year-on-year. However, the underlying price pressures appear sticky, with core inflation accelerating to 4.7% year-on-year. This is one of the reasons why the market continues to price in a fair amount of tightening over 12 months (+183bps), but there is a chance that the central bank will proceed at a more moderate pace after two “oversized” 75bps hikes in a row.

EM Debt Restructuring

The continuing rise in the debt service costs in low-income economies is also concerning, especially in such regions as Sub-Saharan Africa, where sovereign yields widened to 14%+ (J.P. Morgan EMBIG Diversified Africa Index,1 Blended Yield) and countries might be expected to spend close to 3% of GDP on interest payments (on average) going forward. These levels might be prohibitively high, which explains another push towards debt restructuring for poorer nations (including the G20 common framework), as well as creating new facilities and programs to fight poverty and hunger. Stay tuned!

Chart at a Glance: Rising Debt Service Costs

Source: VanEck Research; IMF Fiscal Monitor (October 2022).

1 J.P. Morgan EMBIG Diversified Africa Index tracks total returns for traded external debt instruments issued by emerging market countries in Africa that meet specific liquidity and structural requirements.Follow Us

Related Topics

PMI – Purchasing Managers’ Index: economic indicators derived from monthly surveys of private sector companies. A reading above 50 indicates expansion, and a reading below 50 indicates contraction; ISM – Institute for Supply Management PMI: ISM releases an index based on more than 400 purchasing and supply managers surveys; both in the manufacturing and non-manufacturing industries; CPI – Consumer Price Index: an index of the variation in prices paid by typical consumers for retail goods and other items; PPI – Producer Price Index: a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time; PCE inflation – Personal Consumption Expenditures Price Index: one measure of U.S. inflation, tracking the change in prices of goods and services purchased by consumers throughout the economy; MSCI – Morgan Stanley Capital International: an American provider of equity, fixed income, hedge fund stock market indexes, and equity portfolio analysis tools; VIX – CBOE Volatility Index: an index created by the Chicago Board Options Exchange (CBOE), which shows the market's expectation of 30-day volatility. It is constructed using the implied volatilities on S&P 500 index options.; GBI-EM – JP Morgan’s Government Bond Index – Emerging Markets: comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging market governments; EMBI – JP Morgan’s Emerging Market Bond Index: JP Morgan's index of dollar-denominated sovereign bonds issued by a selection of emerging market countries; EMBIG - JP Morgan’s Emerging Market Bond Index Global: tracks total returns for traded external debt instruments in emerging markets.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Certain information may be provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as the date of this communication and are subject to change. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.

PMI – Purchasing Managers’ Index: economic indicators derived from monthly surveys of private sector companies. A reading above 50 indicates expansion, and a reading below 50 indicates contraction; ISM – Institute for Supply Management PMI: ISM releases an index based on more than 400 purchasing and supply managers surveys; both in the manufacturing and non-manufacturing industries; CPI – Consumer Price Index: an index of the variation in prices paid by typical consumers for retail goods and other items; PPI – Producer Price Index: a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time; PCE inflation – Personal Consumption Expenditures Price Index: one measure of U.S. inflation, tracking the change in prices of goods and services purchased by consumers throughout the economy; MSCI – Morgan Stanley Capital International: an American provider of equity, fixed income, hedge fund stock market indexes, and equity portfolio analysis tools; VIX – CBOE Volatility Index: an index created by the Chicago Board Options Exchange (CBOE), which shows the market's expectation of 30-day volatility. It is constructed using the implied volatilities on S&P 500 index options.; GBI-EM – JP Morgan’s Government Bond Index – Emerging Markets: comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging market governments; EMBI – JP Morgan’s Emerging Market Bond Index: JP Morgan's index of dollar-denominated sovereign bonds issued by a selection of emerging market countries; EMBIG - JP Morgan’s Emerging Market Bond Index Global: tracks total returns for traded external debt instruments in emerging markets.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Certain information may be provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as the date of this communication and are subject to change. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.