Global Pressures – Pick a Direction

November 16, 2022

Read Time 2 MIN

EMEA Political and Policy Risks

There was a global sigh of relief that yesterday’s missile incident in Poland did not result in the further escalation of the Russia/Ukraine war. Central European currencies used this occasion to celebrate, bouncing in the morning trade and topping the EMFX daily “league table”. Some global tension points might have eased lately – we are talking about China’s COVID restrictions and the housing sector support – but geopolitical risks in Europe remain elevated, dampening the growth outlook and slowing the process of disinflation. This is quite problematic, because domestic price pressures show few signs of abating. Today’s microscopic downside surprise in Poland’s core inflation is a case in point – the number might have been a touch lower than expected, but core inflation accelerated to 11% year-on-year in October (which explains why we are uneasy about the planned minimum wage increase and a high likelihood of higher pre-election spending). Against this backdrop, the central bank’s aversion to additional rate hikes makes local yields less attractive relative to peers.

Brazil Fiscal Outlook

A pre-election spending spree is a legitimate concern anywhere in the world, but in Brazil the market is fretting about the post-election’s fiscal largesse. President-elect Luiz Inácio Lula da Silva is lobbying for the removal of a major social program from the spending cap for a number of years, which might help to maintain decent fiscal “optics”, but it will still create extra stimulus in the economy. The central bank is watching the situation like a hawk, and the market thinks there is a chance of it delivering a “warning shot” in the form of a small rate hike in the next 3-4 months. Fiscal concerns are weighing on Brazil’s local bonds, which underperformed GBI-EM peers by a wide margin in the past week.

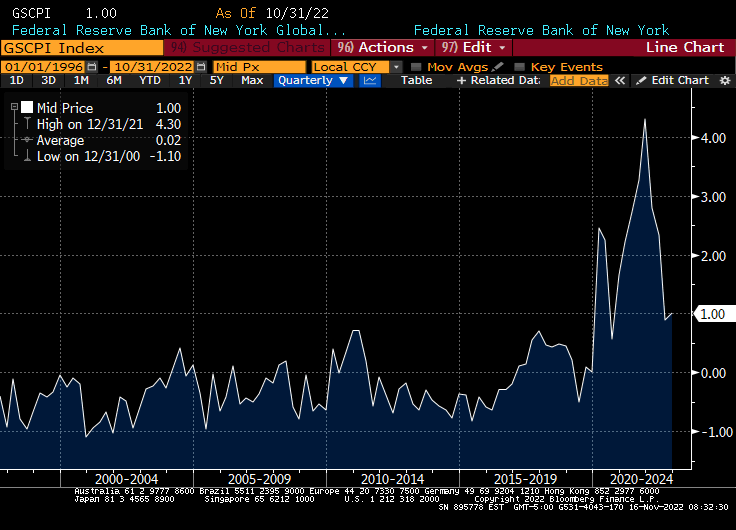

Global Supply Chains

One question that we have is whether EM (and DM) policy “offenders” can be saved by the rapidly easing global supply chain disruptions (see chart below). The latest reports suggest that the improvements are broad-based, which might be a tailwind for the growth outlook (including rebuilding inventories). Easing supply bottlenecks can also lower input prices and reduce some headline inflation pressures going forward. Stay tuned!

Chart at a Glance: Global Supply Chain Pressures? What Pressures?*

Source: Bloomberg LP.

* GSCPI Index: Global Supply Chain Pressure Index seeks to measure supply chain conditions, created by the Federal Reserve. The index combines variables from several indices in transportation and manufacturing.

Follow Us

Related Topics

PMI – Purchasing Managers’ Index: economic indicators derived from monthly surveys of private sector companies. A reading above 50 indicates expansion, and a reading below 50 indicates contraction; ISM – Institute for Supply Management PMI: ISM releases an index based on more than 400 purchasing and supply managers surveys; both in the manufacturing and non-manufacturing industries; CPI – Consumer Price Index: an index of the variation in prices paid by typical consumers for retail goods and other items; PPI – Producer Price Index: a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time; PCE inflation – Personal Consumption Expenditures Price Index: one measure of U.S. inflation, tracking the change in prices of goods and services purchased by consumers throughout the economy; MSCI – Morgan Stanley Capital International: an American provider of equity, fixed income, hedge fund stock market indexes, and equity portfolio analysis tools; VIX – CBOE Volatility Index: an index created by the Chicago Board Options Exchange (CBOE), which shows the market's expectation of 30-day volatility. It is constructed using the implied volatilities on S&P 500 index options.; GBI-EM – JP Morgan’s Government Bond Index – Emerging Markets: comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging market governments; EMBI – JP Morgan’s Emerging Market Bond Index: JP Morgan's index of dollar-denominated sovereign bonds issued by a selection of emerging market countries; EMBIG - JP Morgan’s Emerging Market Bond Index Global: tracks total returns for traded external debt instruments in emerging markets.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Certain information may be provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as the date of this communication and are subject to change. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.

PMI – Purchasing Managers’ Index: economic indicators derived from monthly surveys of private sector companies. A reading above 50 indicates expansion, and a reading below 50 indicates contraction; ISM – Institute for Supply Management PMI: ISM releases an index based on more than 400 purchasing and supply managers surveys; both in the manufacturing and non-manufacturing industries; CPI – Consumer Price Index: an index of the variation in prices paid by typical consumers for retail goods and other items; PPI – Producer Price Index: a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time; PCE inflation – Personal Consumption Expenditures Price Index: one measure of U.S. inflation, tracking the change in prices of goods and services purchased by consumers throughout the economy; MSCI – Morgan Stanley Capital International: an American provider of equity, fixed income, hedge fund stock market indexes, and equity portfolio analysis tools; VIX – CBOE Volatility Index: an index created by the Chicago Board Options Exchange (CBOE), which shows the market's expectation of 30-day volatility. It is constructed using the implied volatilities on S&P 500 index options.; GBI-EM – JP Morgan’s Government Bond Index – Emerging Markets: comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging market governments; EMBI – JP Morgan’s Emerging Market Bond Index: JP Morgan's index of dollar-denominated sovereign bonds issued by a selection of emerging market countries; EMBIG - JP Morgan’s Emerging Market Bond Index Global: tracks total returns for traded external debt instruments in emerging markets.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Certain information may be provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as the date of this communication and are subject to change. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.