Can Wells Fargo, Boeing and Biogen Add Value?

15 October 2020

I’ve written frequently about market valuation in recent months, and for good reason. It’s no secret that a small number of stocks have accounted for a disproportionate amount of the market’s return. More and more U.S. stock investors are facing a difficult decision: do you stay on benchmark and seek little or no alpha, or do you underweight mega-cap, big tech stocks in favor of other potential opportunities in the market?

The risk of allocating to off-benchmark exposure has rewarded far fewer than it has punished over time, particularly in large cap U.S. stocks where the market is arguably most efficient. S&P Dow Jones Indices recently released their SPIVA® (S&P Indices Versus Active) results for Q2 2020 and found that for the trailing five years, far more actively managed U.S. large cap funds underperformed the S&P 500 Index than outperformed. Through 30 June 2020, 78% of funds underperformed for the five-year trailing period, 71% underperformed for the three-year trailing period, and 63% of funds underperformed for the one-year trailing period. That last stat is notable because well over half of active large cap funds failed to outperform the S&P 500 Index in a period that included significant market volatility, an environment where active management supposedly has the upper hand.

For the one-, three-, and five-year period cited in the SPIVA report, the Morningstar® Wide Moat Focus IndexSM (the “Index”) outperformed the S&P 500 Index, though there has been underperformance in certain periods, e.g. in the last three months driven by stock selection in several sectors, most notably industrials and tech.

Average Annualized Return (%)

As of 30 June 2020

| 1 Year | 3 Years | 5 Years | |

| Morningstar Wide Moat Focus Index | 10.49 | 11.78 | 13.47 |

| S&P 500 Index | 7.51 | 10.73 | 10.72 |

As of 30 September 2020

| 3 Months | 1 Year | 3 Years | 5 Years | |

| Morningstar Wide Moat Focus Index | 4.64 | 10.73 | 12.67 | 16.60 |

| S&P 500 Index | 8.93 | 15.15 | 12.28 | 14.14 |

Source: Morningstar. Returns for periods over one year have been annualized. Past performance is no guarantee of future results. An investor cannot invest directly in an index.

Impact of Moats and Valuations

Despite near-term headwinds, Morningstar’s valuation-driven investment philosophy has delivered outperformance versus the broad market since its inception in February 2007. Morningstar strategist, Andrew Lane, recently published a paper examining the impact of the Index’s three primary methodology features: economic moats, equal weighting and valuations. Over its history, each of these three features has incrementally improved the Index’s annualized outperformance.

First, and not uncommon in the market, the Index applies an equal-weighted approach, which allows each Index constituent to contribute to its total return as opposed to those indexes that favor larger, more liquid companies. Next, and more difficult to replicate, is Morningstar’s proprietary economic moat ratings and fair value assessments. Companies that receive Morningstar’s wide economic moat rating are members of an exclusive club that possess competitive advantages that Morningstar believes will allow them to maintain returns on invested capital in excess of their weighted average cost of capital for 20 or more years into the future.

However, Morningstar doesn’t necessarily view economic moat ratings as predictive of performance. Because wide moat companies are widely sought by investors, they tend to trade at higher multiples and are often difficult to find “on sale,” as Lane puts it. This is where Morningstar’s valuation framework comes in: the Index targets those wide moat companies trading at attractive valuations. This combination of equal weighting, wide economic moat ratings and attractive valuations is what has driven excess returns throughout the Index’s history.

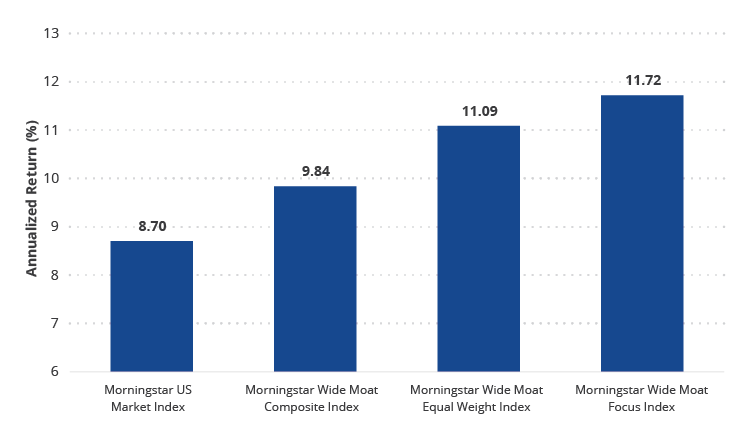

Long-Term Outperformance vs Broad U.S. Market Driven by Moats, Valuations and Equal Weighting

Annualised Total Return 14/2/2007 – 30/9/2020

Source: Morningstar. Morningstar Wide Moat Focus Index inception date is 14/2/2007. Morningstar US Market Index represents 97% of US stock market capitalization. Morningstar Wide Moat Composite Index is a market-capitalization weighted index of all US wide moat companies. Morningstar Wide Moat Equal Weight Index is an equal-weighted index of all US wide moat companies. An investor cannot invest directly in an index.

Top Valuation Opportunities

With valuations top of mind, it’s worth highlighting a few of the most undervalued stocks in the Index. If Morningstar’s conviction is rewarded by way of the market realizing its current mispricing and stock prices rising toward fair value, the Index will benefit.

Wells Fargo & Co. (WFC): 48% Discount to Fair Value

Wells Fargo is a great example of a long-time index constituent that hasn’t been removed or seen its position scaled back in years. It was added in June 2016 and has remained since. This points to the persistent relative attractiveness of its market price relative to its Morningstar-assigned fair value. It is also one of the more commonly cited companies in questions we receive here at VanEck from investors and prospective investors. The bank has been subject to years of negative headlines, but according to Morningstar, it remains one of the top deposit gatherers in the U.S. The bank has easily out-earned its cost of equity for decades and continues to do so today, and Morningstar considers its wide moat rating to be stable.

Wells Fargo earns its wide moat rating based on cost advantages and switching costs. Morningstar cites the bank’s size and leading market share in many business units in which it competes. It has the largest retail branch network in the U.S., aiding its deposit gathering success. Its cost advantages stem from a low-cost deposit base, excellent operating efficiency and conservative underwriting. Notably, Wells Fargo fared better than many of its peers during the global financial crisis.

As of 2 October 2020, Wells Fargo was trading at a 48% discount to its $46 per share fair value estimate, assigned by Morningstar. This is despite a decrease in the bank’s fair value from $50 per share in mid July 2020, following earnings results and factoring a 50% chance of a Biden victory in November and implementation of his proposed tax plan. Morningstar believes the bank will face short- and mid-term headwinds by way of long-term low interest rates, fee income pressures, and potential increases in pandemic-driven credit losses. However, it also believes the bank will focus heavily on cutting expenses in 2021 and 2022, warranting its fair value assessment.

Boeing Co. (BA): 37% Discount to Fair Value

Boeing has also generated its fair share of headlines in recent months. It was a notable addition to the Index in March when it was trading at an all-time low of approximately 70% discount to its Morningstar fair value estimate. The aerospace and defense firm saw its Index weight increased in June because it remained attractively priced at the time.

As of 2 October 2020, Boeing traded at a 37% discount to its $264 per share Morningstar fair value estimate. Its fair value reflects an assumption by Morningstar that Boeing will receive an updated airworthiness directive from the FAA for its 737 MAX model early in the fourth quarter of 2020. The harder variable to predict is the impact the global pandemic will have on commercial airlines. Morningstar believes severe near-term decline in revenue will be followed by a sharp rebound in air traffic after a COVID-19 vaccine is available and well-distributed by mid-2021.

Due to the grounding of the 737 MAX, a demand backlog exists. Morningstar believes an industry shift toward narrow body aircrafts (737 MAX is a narrow body aircraft) will increase in the near term as wide-body aircraft demand recovers more slowly because of their use in longer haul trips, which will require a reliable vaccine before returning to pre-pandemic levels.

Biogen Inc. (BIIB): 29% Discount to Fair Value

Biogen has been an Index constituent since December 2015, though its weighting has scaled down and back up at various times based on changing valuation dynamics. Its current discount isn’t its lowest historically, but it is currently quite undervalued according to Morningstar.

Biogen earns a wide moat rating from its specialty-market-focused portfolio and novel, neurology-focused pipeline. Its leadership in multiple sclerosis (MS) and neurodegenerative diseases paired with its oncology collaboration with Roche have driven returns on invested capital above its cost of capital, and Morningstar forecasts they will remain well above for at least another 10 years.

Biogen’s fair value estimate was decreased in June from $413 per share to $389 per share, reflecting Morningstar’s Tecfidera (MS treatment) forecast paired with increases to expected generic competition following industry litigation. Much of Biogen’s fair value estimate is predicated on pipeline approvals in various segments, some of which are currently expected to be delayed based on recent coronavirus-related treatment delays.

VanEck Morningstar US Wide Moat UCITS ETF (MOAT) seeks to replicate as closely as possible, before fees and expenses the price and yield performance of the Morningstar Wide Moat Focus Index.

Important Disclosure

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

VanEck Asset Management B.V., the management company of VanEck Morningstar US Sustainable Wide Moat UCITS ETF (the "ETF"), a sub-fund of VanEck UCITS ETFs plc, is a UCITS management company under Dutch law registered with the Dutch Authority for the Financial Markets (AFM). The ETF is registered with the Central Bank of Ireland, passively managed and tracks an equity index. Investing in the ETF should be interpreted as acquiring shares of the ETF and not the underlying assets. Investors must read the sales prospectus and key investor information before investing in a fund. These are available in English and the KIIDs/KIDs in certain other languages as applicable and can be obtained free of charge at www.vaneck.com, from the Management Company or from the following local information agents:

UK - Facilities Agent: Computershare Investor Services PLC

Austria - Facility Agent: Erste Bank der oesterreichischen Sparkassen AG

Germany - Facility Agent: VanEck (Europe) GmbH

Spain - Facility Agent: VanEck (Europe) GmbH

Sweden - Paying Agent: Skandinaviska Enskilda Banken AB (publ)

France - Facility Agent: VanEck (Europe) GmbH

Portugal - Paying Agent: BEST – Banco Eletrónico de Serviço Total, S.A.

Luxembourg - Facility Agent: VanEck (Europe) GmbH

Morningstar® US Sustainability Moat Focus Index is a trade mark of Morningstar Inc. and has been licensed for use for certain purposes by VanEck. VanEck Morningstar US Sustainable Wide Moat UCITS ETF is not sponsored, endorsed, sold or promoted by Morningstar and Morningstar makes no representation regarding the advisability in VanEck Morningstar US Sustainable Wide Moat UCITS ETF.

Effective December 17, 2021 the Morningstar® Wide Moat Focus IndexTM has been replaced with the Morningstar® US Sustainability Moat Focus Index.

Effective June 20, 2016, Morningstar implemented several changes to the Morningstar Wide Moat Focus Index construction rules. Among other changes, the index increased its constituent count from 20 stocks to at least 40 stocks and modified its rebalance and reconstitution methodology. These changes may result in more diversified exposure, lower turnover and longer holding periods for index constituents than under the rules in effect prior to this date.

It is not possible to invest directly in an index.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.