ETF 102: The Inner Workings of ETF Creations and Redemptions

20 August 2019

Although the creation and redemption of ETF shares takes place largely behind the scenes for most investors, the process is a defining feature of the ETF structure.

ETF 101: Understanding the Basics

ETF 102: The Inner Workings of ETF Creations and Redemptions

ETF 103: Is This ETF Right for Your Portfolio?

ETF 104: Getting the Most Out of Your ETF Trades

ETF 105: Gaining Efficient Access to Bond Markets with Fixed Income ETFs

Setting the Stage

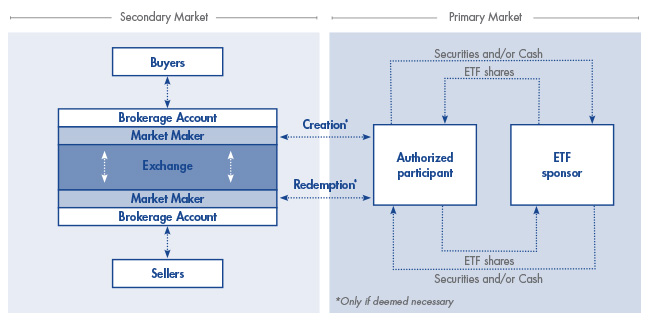

As a starting point, let’s discuss the differences between the secondary and primary markets for ETF shares.

The secondary market, which includes the widely recognised securities exchanges, is where investors buy and sell existing shares of ETFs. For example, if you wish to buy 2,000 shares of an ETF, you typically place an order through your brokerage account and purchase those shares at market price from other sellers in the secondary market.

The primary market refers to where ETF share creations and redemptions take place in large specified units. It provides an additional “layer”, or source, of liquidity that can be accessed for large orders or when demand exceeds supply, or vice versa, on the secondary market. Typically, large financial institutions, authorised participants, and market makers1 transact in the primary market. Market makers buy and sell ETF shares in the secondary market to provide liquidity and may also serve as authorised participants.

Authorised Participants

Authorised participants (APs) are an important part of the creation and redemption process. To create new passively managed ETF shares, the AP generally acquires shares in all of the underlying securities that compose the ETF, in the same proportions as the fund’s index. To create new ETF shares the AP will deliver all of the underlying securities that compose the ETF or the equivalent cash amount and in exchange, receives shares of the ETF in blocks known as creation units. The AP then sells these ETF shares in the secondary market. The additional supply of shares tends to bring the ETF’s price back in line with its NAV2.

Carefully Crafted Creations

When there are not enough ETF shares available on the secondary market to satisfy demand, an ETF may begin trading at a premium (its current market price is higher than its NAV). When this happens, an AP may step in and create new shares.

To create new passively managed ETF shares, the AP generally acquires shares in all of the underlying securities that compose the ETF, in the same proportions as the fund’s index. On the primary market, the AP then delivers this basket of securities to the ETF issuer, and in exchange, receives shares of the ETF in blocks known as creation units3. The AP then sells these ETF shares in the secondary market. The additional supply of shares tends to bring the ETF’s price back in line with its NAV.

Road to Redemptions

The process described above also works in reverse when demand is low. For example, let us imagine that an ETF begins trading at a discount (its current market price is lower than its NAV). The AP leaps into action, buying shares of the discounted ETF on the secondary market and tendering these shares to the issuer for shares of the ETF’s underlying securities.

Redemptions reduce the number of ETF shares available on the secondary market. As a result, the discount shrinks or disappears as the ETF share price moves closer in line with its NAV.

Sources of Liquidity

So, there are actually two primary sources of ETF liquidity: the secondary or open market, consisting of shares bought and sold throughout the day, and the primary market managed by APs. Most ETF investors rely on secondary market liquidity.

Primary market liquidity draws on the liquidity of the underlying securities comprising the ETF. Very large trades can tap into the deeper liquidity source of the primary market, where large blocks of ETF shares can be either created or redeemed.

In Summary

Creations and redemptions are critical to the structure and liquidity of ETFs. Through this mechanism the supply of ETF shares in the open market can be brought in line with demand, thus fairly pricing ETFs.

-----------------------------------------------------------------------

1Market makers: Specialised traders who seek liquidity for a set of securities on an exchange.2Net Asset Value (NAV): The total value per share of an ETF’s underlying securities, less its liabilities.

3Creation unit: Large blocks of ETF shares created by ETF issuers. Creation unit sizes can vary by issuer and fund.

Important Disclosure

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.