Global Recession Narrative - Policy Dilemma

23 June 2022

Read Time 2 MIN

Global Recession Fears

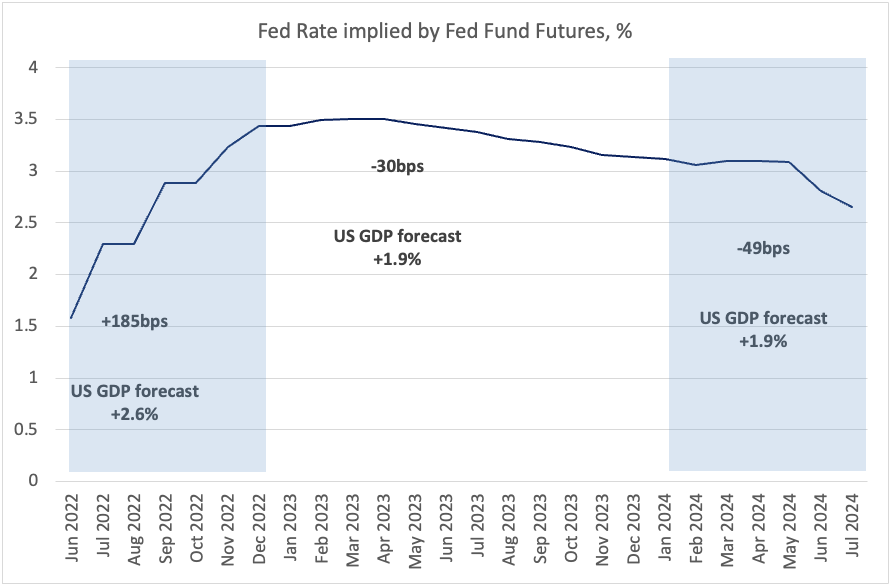

Weak European activity gauges (Purchasing Managers Indices, PMI) reinforced growth concerns in the region this morning. The subsequent below-consensus PMI prints in the U.S. gave an extra boost to the global recession narrative, leading to a massive rally in U.S. Treasuries and European rates (including Central Europe). The consensus growth forecast for both regions (Europe and the U.S.) still looks rosy 1-2 years ahead (around 2%), but the market expectations for the policy rate in the U.S. (Fed Fund Futures) tell a less optimistic growth story, anticipating that the current tightening cycle will end in December and seeing rate cuts from H2-2023 on (see chart below).

Pace of Rate Hikes in EM

This macro backdrop creates additional policy challenges for emerging markets (EM), where tightening is already well underway, but inflation pressures are not yet abating. Central banks in Chile (CLP) and Brazil (BCB) believe that aggressive rate hike frontloading gave them room to proceed at a slower pace from now on. However, Mexico might not have such luxury yet. The latest bi-weekly inflation prints – both headline and core – surprised significantly to the upside (respective 7.88% and 7.47% year-on-year), moving further away from the target (2-4%), and cementing the consensus expectation of a 75bps rate hike this afternoon (with a small probability of a larger 100bps move).

Monetary Policy Room in EM Asia

One EM region that can afford to proceed gradually with policy normalization is EM Asia. Regional headline inflation is much closer to the official targets than either in EMEA and LATAM, and even within the target range in two countries (China and Indonesia). This explains why the Indonesian central bank (BI) chose to stay on hold earlier today (after adjusting the reserve requirements for banks higher in May, and hoping that fiscal subsidies will cap inflation pressures), and why the Philippine central bank (BSP) raised its policy rate only by 25bps. The regional focus now shifts to Thailand, which refused to hike - the policy rate is still at 0.5%! - despite annual headline inflation surging to 7.1%. The next rate-setting meeting is in August, and we strongly suspect that another “oversized” inflation print will change the doves/hawks balance at the central bank. Stay tuned!

Chart at a Glance: Fed Fund Futures – Anticipating Recession?

Source: VanEck Research; Bloomberg LP

Related Insights

IMPORTANT DEFINITIONS & DISCLOSURES

This material may only be used outside of the United States.

This is not an offer to buy or sell, or a recommendation of any offer to buy or sell any of the securities mentioned herein. Fund holdings will vary. For a complete list of holdings in VanEck Mutual Funds and VanEck ETFs, please visit our website at www.vaneck.com.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.