Gold’s Misguided ESG Ratings

12 February 2020

Read Time 4 MIN

Geopolitical Events Support Gold

Gold started the year driven by risks associated with geopolitical events. On January 3, a U.S. drone attack on an Iranian general in Iraq led to a retaliatory strike by Iran on a U.S.-Iraq military base on January 8. This enabled gold to briefly reach the $1,600 per ounce level for the first time since 2013. Gold pulled back to its low for the month on January 14, but then trended higher with news of the Coronavirus outbreak in China. Metals and crude oil prices fell sharply as the virus spread and markets worried about impacts on economic growth in China and beyond. U.S. treasuries rallied and gold finished the month with a $71.89 per ounce (4.7%) gain at $1,589.16. Meanwhile, gold stocks underperformed gold, probably due to some mean reversion following strong outperformance in December.

Gold Price not Indicative of Physical Demand

The World Gold Council (WGC) reported that total gold demand fell 1% in 2019. Consumer demand for jewelry, bars, and coins was especially weak, falling 11% to a decade low, mainly due to weakness in India and China. Given the decline in demand, how is it that the gold price was able to advance 18% in 2019? It’s because gold behaves more like a financial asset than a commodity. Physical demand drives commodities prices, whereas financial demand drives gold prices. Strong buying from bullion exchange traded products and central banks for gold as a financial and currency hedge drove the price, even though the volumetrically larger consumer demand was very weak. Investment demand in the paper market (futures and over-the-counter) also contributed to gains in 2019. We expect the same demand and price relationships to persist in 2020 if gold price strength continues. It currently looks like gold is poised to trend through $1,600 per ounce in the first half of the year.

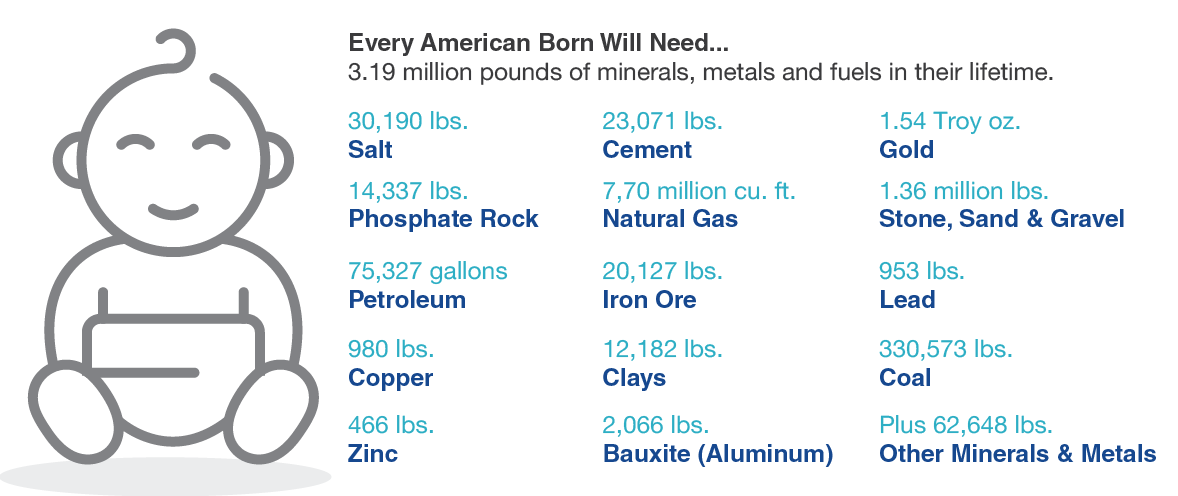

ESG Movement Emerges as Lifestyle Demands Fuel Pollution

Around the world, most people, organizations, corporations and governments have finally come to realize that there is too much pollution of all types and that the planet would be a better place if there was less of it. Our lifestyles are the fundamental drivers of pollution. The cartoon below shows the average American will consume over 3 million pounds of the minerals, metals and fuels needed to manufacture and build virtually everything around us. Europeans and Japanese consume a similar amount, while there are billions of others who aspire to attain the same wealth and conveniences as people in developed countries. Extracting and consuming such quantities creates pollution, but who is willing to give up his or her flat-screen, car or vacation in order to reduce their carbon footprint?

There is a tremendous amount of discussion, controversy and politics around the impact that pollution will have on the environment in the future. Out of this has emerged a broad-based movement to mitigate the threat that pollution poses. In finance, this movement is known as ESG (Environment/Social/Governance) investing. According to Bloomberg, assets invested using a broad definition of this approach reached $30.7 trillion at the start of 2018.

ESG investing has the best intentions, however, within the gold industry, we believe it carries many shortcomings as it is currently being used. ESG ratings agencies score and rank companies based on their ESG performance. These agencies are becoming powerful gatekeepers as a growing number of investors use ESG ratings to screen companies for further consideration. Unfortunately, the precious metals industry ranks among the riskiest due to its environmental and social exposure. Unlike most industries, mining companies cannot choose the climate, community or location that is best suited for their business. They must build in and around their ore deposits, which are essentially scattered randomly around the world and usually in very remote places. Mining is also capital intensive, requiring more heavy equipment, material and energy than most businesses. Therefore, we believe for an investor to compare the ESG performance of a mining company to a retailer, aerospace, or semiconductor company is disingenuous. Generally, the closer a sector is to the consumer or end-user, the lower the ESG risk. However, in our view no other sector could exist without the basic materials that mining provides.

Gold Industry Sets Global ESG Principles

Each gold operation has hundreds of environmental and social criteria and many are unique to each operation. Gold companies we have spoken to engage regularly with the ratings agencies. However, they are concerned that the huge volume of ESG information is overwhelming and that the agencies lack the capacity or expertise to do an adequate evaluation. There are also concerns that ratings agencies have an over-reliance on press and internet articles and non-governmental organizations (NGO) reports for information. We believe these often carry a negative bias against mining and lack a balanced third-party perspective. In addition, there is a “black box” aspect and lack of standardization as to how each agency arrives at their rankings. For example, Sustainalytics describes the core of their model as “a list of subindustry ‘Beta Indicators’ that generate so-called ‘Beta Signals’ that finally get added to the subindustry default beta value of 1 together with the Qualitative Overlay and the Correction Factor.” We doubt there are many investors that can relate to this description.

Current ESG ratings analysis also ignores the contribution mining has made to thousands of communities around the world. Mining creates jobs and brings health care and education to lesser developed countries where we believe few businesses or charities would operate. In places like Nevada, Western Australia or Canada, mining supports much of the rural economy, lifestyle and culture. We believe that any ESG analysis must incorporate on-the-ground performance, in addition to the checklists and public information used by ratings agencies.

The gold industry has recognized the need for rigor and standardization in ESG reporting. To accomplish this, in 2019 the industry-backed WGC published Responsible Gold Mining Principles (RGMP). The RGMP sets ten ESG principles containing 51 items for companies to report on. The principles are a synthesis of a number of global standards already in use as well as input from a range of stakeholders and agencies. They are aimed at providing investor and consumer confidence that gold is ethically sourced. Conformance with the principles will be insured annually through public reporting and a third party “independent assurance” conducted at both the mine site and corporate level. Companies that participate will be allowed a three-year period of implementation, with independent assurance beginning in the third year. We expect all of the gold producers in which we invest to adopt RGMP.

The WGC has also set a lofty goal of net-zero emissions by 2050 through process enhancement, decarbonisation of transport and electricity, self-sufficient energy and emissions off-sets. While the industry is already reducing emissions where it makes the most economic sense, in our opinion, meeting the 2050 goal will require further technical advances in renewable energy, battery storage and electric vehicles that are beyond the gold industry’s control. Companies stand ready to test and adopt new technologies, but we believe widespread implementation is years from becoming reality.

Managing environmental and social risk is nothing new to gold companies. In fact, it is among the most important aspects of their business. We do not invest in companies that fail to strive for ESG excellence. However, if investors avoid the broader mining industry due to what we see as unrealistic or misguided ESG expectations, the industry may become starved of capital needed to maintain production. If taken to extreme, we believe a lack of capital creates shortages and rising prices that could bring an unwanted inflationary cycle with world-wide economic hardship.

Related Insights

IMPORTANT DEFINITIONS & DISCLOSURES

This material may only be used outside of the United States.

This is not an offer to buy or sell, or a recommendation of any offer to buy or sell any of the securities mentioned herein. Fund holdings will vary. For a complete list of holdings in VanEck Mutual Funds and VanEck ETFs, please visit our website at www.vaneck.com.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.