Peak Inflation = Peak Rates?

26 July 2022

Read Time 2 MIN

Brazil Inflation, Frontloading

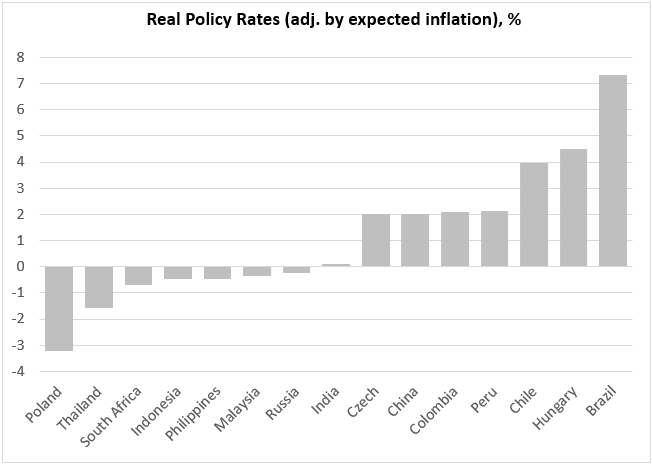

Moderating mid-month inflation in Brazil gave us hope that peak-inflation might actually be real. Headline inflation eased a tiny bit more than expected to 11.39% year-on-year – an encouraging sign for the consensus expectations that see inflation falling to 8.5% by the end of the year and further to 6% in 12 months. For this scenario to materialize, it is important that (a) the inflation diffusion index continues to go down, and (b) the government does not get carried away by its fiscal successes and stops expanding its spending plans. If this happens, Brazil would have by far the highest real policy rate among major emerging markets (EM) (see chart below), which should give it plenty of space to finish its tightening cycle in September, and maybe start thinking about rate cuts sometime in 2023.

EM Real Policy Rates

The most incredible point about the chart below is not Brazil’s sky-high real policy rate, but that it is followed by Hungary, which until recently was among EM policy laggards. And it was duly punished by the market, having posted the second worst local debt return so far this year (in the J.P. Morgan’s GBI-EM Index). But if you have the same inflation as in Brazil (11.7% year-on-year), perhaps your central bank should adopt Brazil’s response function – which means aggressively frontloading rate hikes. Hungary did not disappoint today, raising its policy rate by 100bps more (after a double punch of +185bps and +200bps). So, Hungary’s policy rate is now in double digits for the first time since the global financial crisis of 2008/09 – and, as we just said, the real policy rate adjusted by expected inflation is now the second highest in EM. This created a significant policy cushion, but it’s absolutely critical to proceed with fiscal adjustment, as spending got a bit out of control in the run up to the elections.

Terminal Rates in DM

The notion of peak rates features prominently in developed markets (DM) discussions as well. Today’s weaker than expected Conference Board consumer confidence index in the U.S. raised additional concerns about the Q3 growth headwinds – right in the run up to the U.S. Federal Reserve’s (Fed’s) meeting tomorrow. The expectation (measured by the Fed Funds Futures) is still for a 75bps rate hike, but the market sees no additional hikes after December. A series of downside activity surprises in the Eurozone – and negative headlines about the Russian gas exports’ disruptions – depressed the market expectations for the European Central Bank (ECB), which is now expected to take a pause after March 2023. Stay tuned!

Chart at a Glance: Real Policy Rates in EM – Some Central Banks Get It

Source: VanEck Research; Bloomberg LP

Related Insights

IMPORTANT DEFINITIONS & DISCLOSURES

This material may only be used outside of the United States.

This is not an offer to buy or sell, or a recommendation of any offer to buy or sell any of the securities mentioned herein. Fund holdings will vary. For a complete list of holdings in VanEck Mutual Funds and VanEck ETFs, please visit our website at www.vaneck.com.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.