Pivot-Ready?

January 27, 2023

Read Time 2 MIN

EM Tightening Cycles

One of this week’s lessons is that many emerging markets (EM) central banks do not act as pivot-ready as the market expects – even in places where disinflation is already underway and growth is clearly slowing. South Africa’s split decision yesterday (with two out of three board members voting for a 50bps hike) is a good example. Thailand’s central bank also sent a hawkish message earlier this week (as a backdrop for a 25bps rate hike). Hungary’s central bank raised the reserve requirements for banks (as the effective policy rate is already around 16%). The Chilean central bank stayed on hold yesterday, but its statement drew attention to a wide gap between inflation and the target. Today’s rate-setting meeting in Colombia and the next week’s policy rate decision in Brazil will also be closely watched (these countries account for about 14% of the J.P. Morgan’s EM local bond index). Brazil’s policy uncertainty (especially on the fiscal front) and unhelpful comments about the central bank’s independence keep many investors on the sidelines.

FED Rate Expectations

So, the best way to describe EM central banks’ policy stance is “prudent” rather than “pivot-ready”. What about their developed markets (DM) counterparts? We do not have to wait for much longer – both the U.S. Federal Reserve and the ECB are meeting next week, and today’s Personal Consumption Expenditure prints in the U.S. looked consistent with the market expectation of a slower pace of hikes (+25bps). But as long as DM hikes continue, EM’s policy cushion (the policy rate differential with DMs) will be getting smaller. The differential between EM local rates and U.S. Treasuries is also narrowing, especially in Asia (J.P. Morgan’s GBI-EM Asia yield-to-maturity is mere 3.95%). One can argue that this reflects China’s reopening, but the trend is not very new and it might signal that the region is truly re-rating – with more “EM Graduates”, orthodox policies, and, yes, tighter spreads.

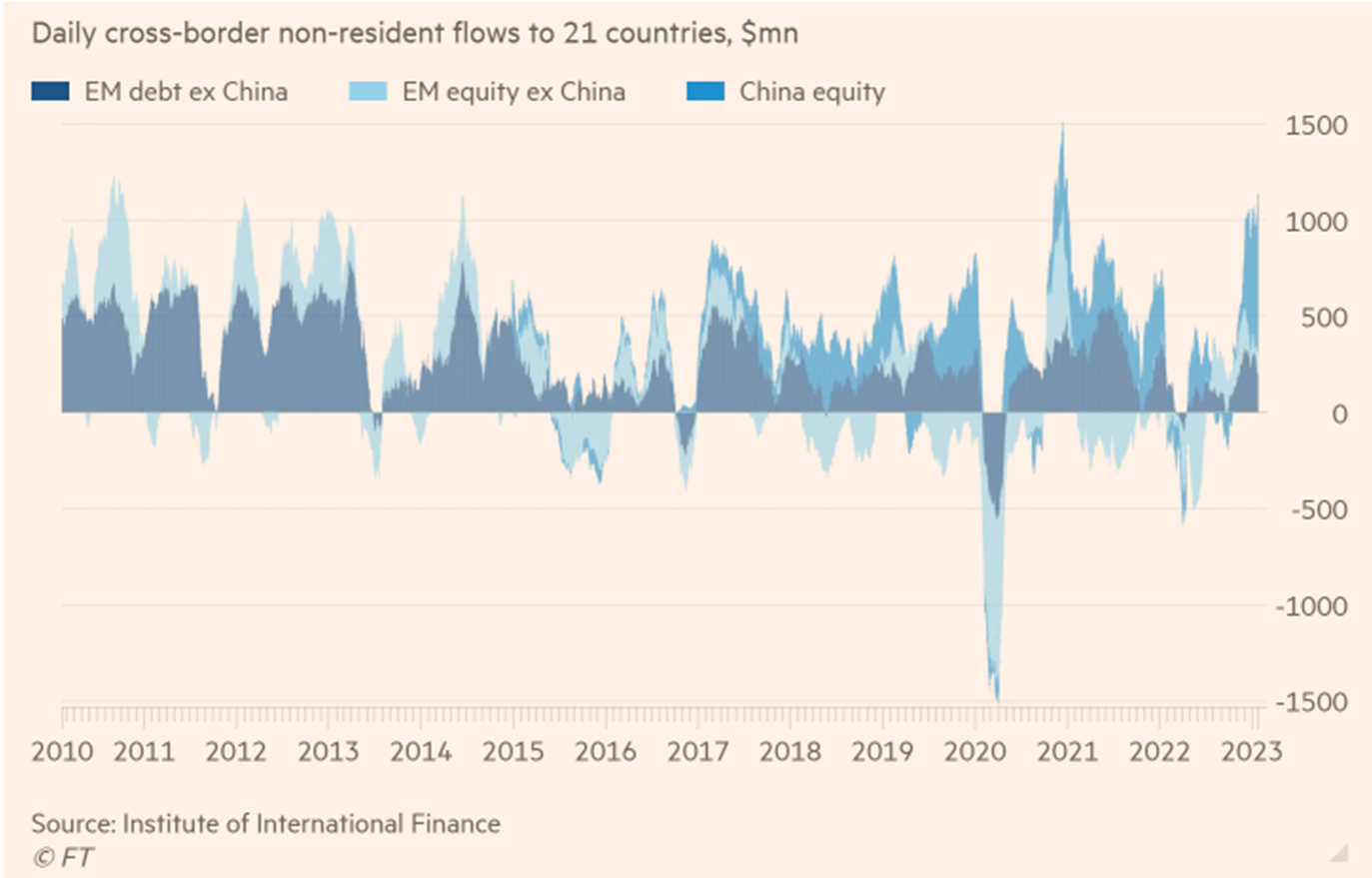

EM Inflows

Massive inflows into EM assets so far this year show that investors are not deterred by the narrowing rate differentials – the China’s reopening/disinflation/softer landing stories being powerful sentiment “boosters” (see chart below). Sell-side surveys show that cash balances are still significant, albeit we are mindful of high EM bond issuance, with many governments using this opportunity to pre-finance their 2023 issuance needs. High EM inflows also reflect expectations of the Fed’s eventual pivot. The Fed does not seem eager to fall in line with this view – would next week be different? Stay tuned!

Chart at a Glance: Huge Pickup in Inflows into EM Assets

Source: Financial Times

Related Topics

Related Insights

Related Topics

Related Insights

February 26, 2024

January 04, 2024

October 27, 2023

PMI – Purchasing Managers’ Index: economic indicators derived from monthly surveys of private sector companies. A reading above 50 indicates expansion, and a reading below 50 indicates contraction; ISM – Institute for Supply Management PMI: ISM releases an index based on more than 400 purchasing and supply managers surveys; both in the manufacturing and non-manufacturing industries; CPI – Consumer Price Index: an index of the variation in prices paid by typical consumers for retail goods and other items; PPI – Producer Price Index: a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time; PCE inflation – Personal Consumption Expenditures Price Index: one measure of U.S. inflation, tracking the change in prices of goods and services purchased by consumers throughout the economy; MSCI – Morgan Stanley Capital International: an American provider of equity, fixed income, hedge fund stock market indexes, and equity portfolio analysis tools; VIX – CBOE Volatility Index: an index created by the Chicago Board Options Exchange (CBOE), which shows the market's expectation of 30-day volatility. It is constructed using the implied volatilities on S&P 500 index options.; GBI-EM – JP Morgan’s Government Bond Index – Emerging Markets: comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging market governments; EMBI – JP Morgan’s Emerging Market Bond Index: JP Morgan's index of dollar-denominated sovereign bonds issued by a selection of emerging market countries; EMBIG - JP Morgan’s Emerging Market Bond Index Global: tracks total returns for traded external debt instruments in emerging markets.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Certain information may be provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as the date of this communication and are subject to change. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.

PMI – Purchasing Managers’ Index: economic indicators derived from monthly surveys of private sector companies. A reading above 50 indicates expansion, and a reading below 50 indicates contraction; ISM – Institute for Supply Management PMI: ISM releases an index based on more than 400 purchasing and supply managers surveys; both in the manufacturing and non-manufacturing industries; CPI – Consumer Price Index: an index of the variation in prices paid by typical consumers for retail goods and other items; PPI – Producer Price Index: a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time; PCE inflation – Personal Consumption Expenditures Price Index: one measure of U.S. inflation, tracking the change in prices of goods and services purchased by consumers throughout the economy; MSCI – Morgan Stanley Capital International: an American provider of equity, fixed income, hedge fund stock market indexes, and equity portfolio analysis tools; VIX – CBOE Volatility Index: an index created by the Chicago Board Options Exchange (CBOE), which shows the market's expectation of 30-day volatility. It is constructed using the implied volatilities on S&P 500 index options.; GBI-EM – JP Morgan’s Government Bond Index – Emerging Markets: comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging market governments; EMBI – JP Morgan’s Emerging Market Bond Index: JP Morgan's index of dollar-denominated sovereign bonds issued by a selection of emerging market countries; EMBIG - JP Morgan’s Emerging Market Bond Index Global: tracks total returns for traded external debt instruments in emerging markets.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Certain information may be provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as the date of this communication and are subject to change. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.