China Growth - Can “Little Giants” Save the Day?

January 31, 2022

Read Time 3 MIN

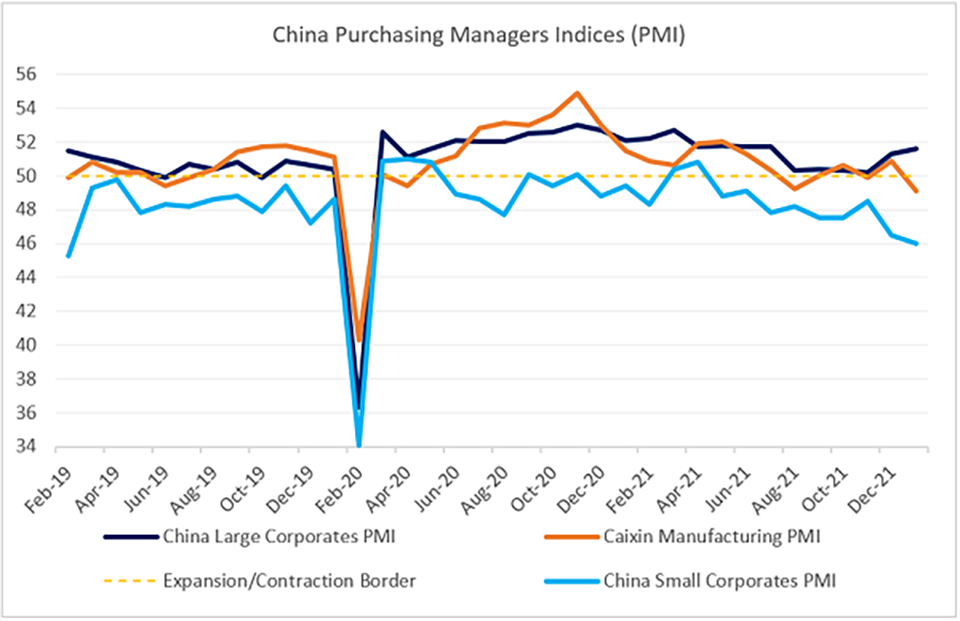

The widening gap between activity gauges for China’s small and large companies call for more targeted policy support, but also draws attention to the efficacy of the current policy mix.

China Growth Engines

China is trying to reignite its growth engines - but can authorities do it with small and privately-owned companies lagging behind? This was our main question following the release of January’s domestic activity gauges. China’s large corporates did relatively well under the circumstances (Omicron wave, zero-COVID policy, Chinese New Year seasonality) - the respective PMI1 rose for the second month in a row to 51.6. However, the small companies PMI fell to the new post-COVID low of 46.0, and the Caixin manufacturing PMI (which has a larger share of private firms) was weaker than expected, and back in contraction zone (see chart below).

China Supply-Side Stimulus and Its Consequences

China’s reliance on SOEs2 and supply-side stimulus produced better (and faster) results early in the pandemic compared to most emerging markets (EM) and developed markets (DM), which focused on demand-side measures. China was able to post positive GDP growth in 2020, and increase its global share of manufacturing and exports. However, some of these factors can become growth headwinds going forward, as the rest of the world reopens, global growth normalizes, and “a wall of liquidity” stimulus dries out. Against this backdrop, depressed consumption - exacerbated by developments in the real estate sector - casts doubts over China’s ability to reaccelerate in the second half of the year and meet its growth target. About 1/4 of analysts participating in Bloomberg’s consensus survey see China growing at less than 5% this year.

China Slowdown and Policy Response

Accommodative policy stance - including both blanket measures (gradual cuts in policy rates and reserve requirements for banks) and targeted stimulus to support specific sectors - appears to be the right near-term policy prescription for China, especially since earlier measures are yet to make the full impact on the economy. The question is whether “more of the same” is the most efficient approach, especially as regards SMEs3. This is the reason why the latest initiative in the SME space - called “Little Giants” - attracted attention. Authorities hope that promoting specialized (or “niche”) manufacturing SMEs would help to support growth and move the economy up the value added chain. It remains to be seen, however, whether “Little Giants” represents a qualitative policy shift, whether small companies will be able to thrive under more state control, and how this will affect China’s shift to consumption-led growth model. Stay tuned!

Chart at a Glance: Widening Gap between China’s Small and Large Company PMIs

Source: Bloomberg LP

11We believe PMIs are a better indicator of the health of the Chinese economy than the gross domestic product (GDP) number, which is politicized and is a composite in any case. The manufacturing and non-manufacturing, or service, PMIs have been separated in order to understand the different sectors of the economy. These days, we believe the manufacturing PMI is the number to watch for cyclicality.

2SOE – State-Owned Enterprise

3SME- Small-Medium Sized Enterprises

Related Topics

Related Insights

Related Topics

Related Insights

February 26, 2024

January 04, 2024

October 27, 2023

PMI – Purchasing Managers’ Index: economic indicators derived from monthly surveys of private sector companies. A reading above 50 indicates expansion, and a reading below 50 indicates contraction; ISM – Institute for Supply Management PMI: ISM releases an index based on more than 400 purchasing and supply managers surveys; both in the manufacturing and non-manufacturing industries; CPI – Consumer Price Index: an index of the variation in prices paid by typical consumers for retail goods and other items; PPI – Producer Price Index: a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time; PCE inflation – Personal Consumption Expenditures Price Index: one measure of U.S. inflation, tracking the change in prices of goods and services purchased by consumers throughout the economy; MSCI – Morgan Stanley Capital International: an American provider of equity, fixed income, hedge fund stock market indexes, and equity portfolio analysis tools; VIX – CBOE Volatility Index: an index created by the Chicago Board Options Exchange (CBOE), which shows the market's expectation of 30-day volatility. It is constructed using the implied volatilities on S&P 500 index options.; GBI-EM – JP Morgan’s Government Bond Index – Emerging Markets: comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging market governments; EMBI – JP Morgan’s Emerging Market Bond Index: JP Morgan's index of dollar-denominated sovereign bonds issued by a selection of emerging market countries; EMBIG - JP Morgan’s Emerging Market Bond Index Global: tracks total returns for traded external debt instruments in emerging markets.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Certain information may be provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as the date of this communication and are subject to change. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.

PMI – Purchasing Managers’ Index: economic indicators derived from monthly surveys of private sector companies. A reading above 50 indicates expansion, and a reading below 50 indicates contraction; ISM – Institute for Supply Management PMI: ISM releases an index based on more than 400 purchasing and supply managers surveys; both in the manufacturing and non-manufacturing industries; CPI – Consumer Price Index: an index of the variation in prices paid by typical consumers for retail goods and other items; PPI – Producer Price Index: a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time; PCE inflation – Personal Consumption Expenditures Price Index: one measure of U.S. inflation, tracking the change in prices of goods and services purchased by consumers throughout the economy; MSCI – Morgan Stanley Capital International: an American provider of equity, fixed income, hedge fund stock market indexes, and equity portfolio analysis tools; VIX – CBOE Volatility Index: an index created by the Chicago Board Options Exchange (CBOE), which shows the market's expectation of 30-day volatility. It is constructed using the implied volatilities on S&P 500 index options.; GBI-EM – JP Morgan’s Government Bond Index – Emerging Markets: comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging market governments; EMBI – JP Morgan’s Emerging Market Bond Index: JP Morgan's index of dollar-denominated sovereign bonds issued by a selection of emerging market countries; EMBIG - JP Morgan’s Emerging Market Bond Index Global: tracks total returns for traded external debt instruments in emerging markets.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Certain information may be provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as the date of this communication and are subject to change. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

Investing in international markets carries risks such as currency fluctuation, regulatory risks, economic and political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility, lower trading volume, and less liquidity. Emerging markets can have greater custodial and operational risks, and less developed legal and accounting systems than developed markets.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.